Access advice to guide your steps

If you've been following the news lately, you've probably heard a lot of noise about capital gains tax and how the government is set to take a bigger slice when Australians sell assets. Some of the headlines have been dramatic; and for larger investors, some of the concern is warranted.

But here's what those headlines consistently miss: if you're a small business owner, a tradie who built a team, a café owner who's given twenty years to a business, a mum-and-dad retailer; there is a completely separate set of tax rules that were designed specifically for you. And under those rules, it's entirely possible to sell your business and pay little or no capital gains tax at all.

This article explains how the small business CGT concessions work, using plain English and two real-world examples.

When you sell something for more than you paid for it, the difference is called a capital gain. The ATO generally wants a share of that gain as tax.

For example: you buy a business for $200,000 and sell it ten years later for $800,000. Your capital gain is $600,000. Without any concessions, that gain gets added to your taxable income for the year, which can mean a very large tax bill.

The general 50% CGT discount (available when you’ve held an asset for more than 12 months) has historically reduced that burden significantly. From 1 July 2027, the Federal Government is replacing that discount with cost base indexation and a new 30% minimum tax on real capital gains, changes that have attracted a lot of attention in the media and on social media. We’ve covered those changes in detail in a separate article. Capital Gains Tax, How it Works, and What's Changing

The good news for small business owners is this: the four small business CGT concessions in the tax law are completely separate to the general discount, and are explicitly not affected by the 2026–27 Budget changes. The Budget Papers confirmed it in plain terms: “The current small business CGT concessions will continue unchanged.” That’s not spin, it’s a direct quote from Budget Paper No. 1.

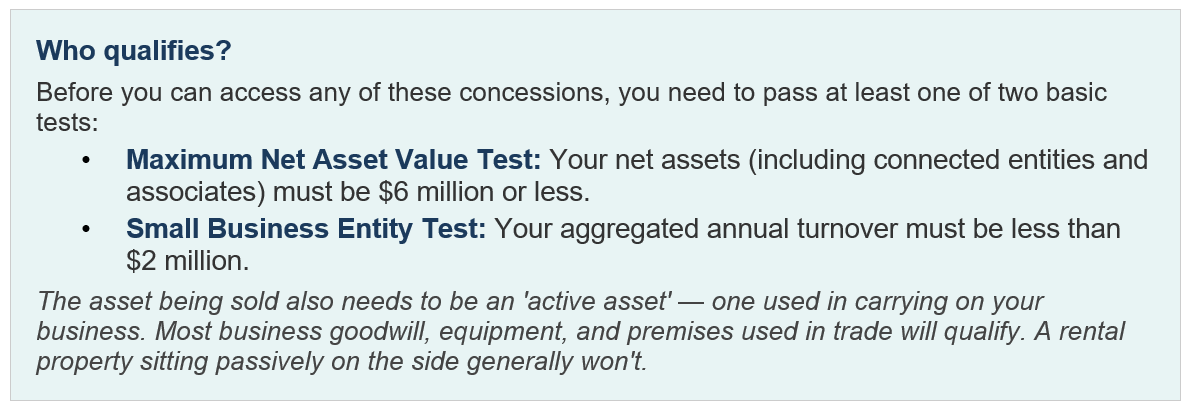

Under Division 152 of the Income Tax Assessment Act 1997, eligible small business owners can access up to four separate concessions when they sell a business asset. These can be used individually or stacked together, and in the right circumstances they can reduce a capital gain to zero.

This is the most powerful concession available. If you've owned your business asset continuously for at least 15 years, are aged 55 or over, and are selling in connection with your retirement (or are permanently incapacitated), your entire capital gain is disregarded. Zero. Gone.

On top of that, you can contribute the sale proceeds into your superannuation under the CGT cap contribution, currently $1,865,000 (FY2026, indexed annually), without it counting against your normal contribution limits. This makes it one of the most effective legal retirement strategies available to a small business owner.

If you don’t meet the 15-year exemption requirements, the 50% active asset reduction can still cut your gain in half. For sales before 1 July 2027, it also stacks with the general 50% CGT discount (if your asset has been held for more than 12 months), meaning the combined effect can reduce your taxable gain to just 25% of the original amount. For sales from 1 July 2027, the general discount is replaced by cost base indexation; but the 50% active asset reduction still applies in full as a separate, independent step. The SB concessions are untouched.

There's no age requirement and no retirement trigger for this concession, it's available to any qualifying small business owner who sells an active asset.

The retirement exemption allows you to shelter up to $500,000 of a capital gain over your lifetime. You don't actually have to be retired to use it, you just need to make the election.

There is one important condition: if you're under 55 at the time you make the election, the exempt amount must be contributed directly into superannuation or a retirement savings account. If you're 55 or over, the super contribution is optional.

The $500,000 is a lifetime limit, not an annual one. If you used $200,000 of this concession when you sold a previous business years ago, only $300,000 remains available to you now.

The rollover concession allows you to defer a capital gain (rather than eliminate it) by rolling the proceeds into a replacement business asset. The gain is parked until you eventually sell the replacement asset.

This is most useful when you're restructuring or moving from one business to another, rather than exiting altogether. The replacement asset needs to be acquired within two years of the sale (or up to one year before it).

Here’s where it gets powerful. The concessions can be applied in order, each one reducing the remaining gain further. For sales before 1 July 2027, the general 50% CGT discount applies first (if eligible), then the 50% active asset reduction, and then the retirement exemption on whatever remains. For sales from 1 July 2027, the general discount is replaced by indexation, but the active asset reduction and retirement exemption still apply in exactly the same way, and can still reduce a gain to zero.

The 15-year exemption is different, if it applies, you apply it instead of the others. There's nothing left to reduce.

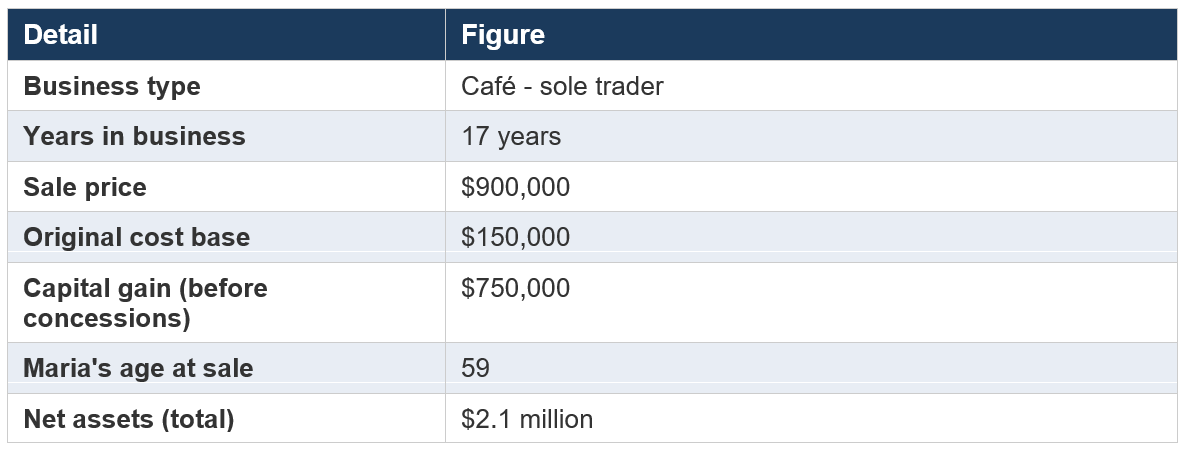

Maria has run her café for 17 years and is ready to retire. Her net assets are well under $6 million and her business clearly qualifies as an active asset.

Yes. She has owned the business for more than 15 years, she is over 55, and she is selling in connection with her retirement.

Result: Her entire $750,000 capital gain is disregarded. No tax is payable.

Maria can contribute the proceeds into superannuation under the CGT cap contribution - up to $1,780,000 - without it counting against her concessional or non-concessional contribution caps. She has the opportunity to significantly boost her retirement savings in a single transaction, in a tax-effective environment.

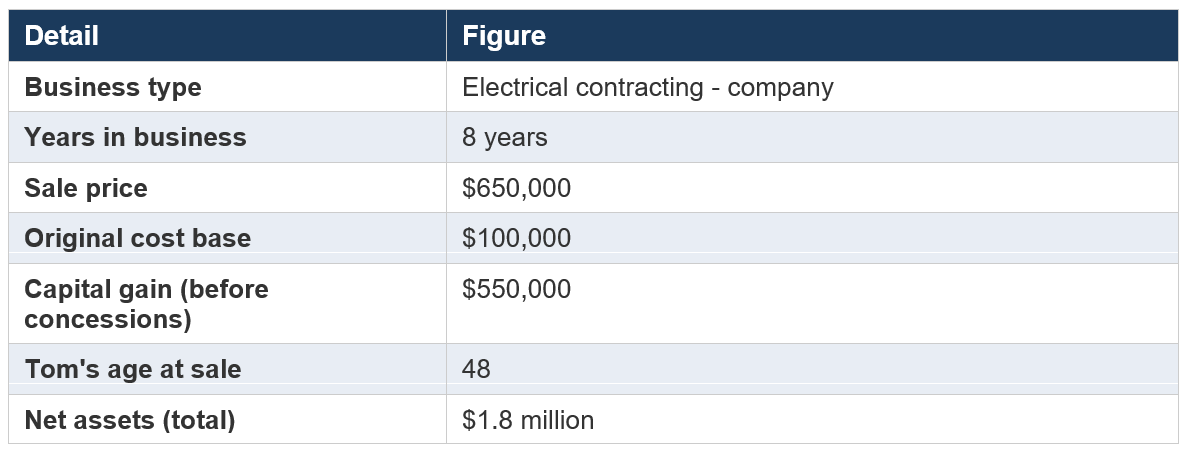

Tom has built a successful electrical contracting business over eight years and has received an offer he can’t refuse. He’s 48, so he doesn’t meet the age requirement for the 15-year exemption - and he’s only held the business for eight years anyway. But he still has meaningful options. This example shows a sale before 1 July 2027 (when the general 50% CGT discount still applies). We’ve also shown what happens for a post-2027 sale below; spoiler: the result is the same.

Tom has held the asset for more than 12 months, so the general discount applies first.

$550,000 × 50% = $275,000 remaining gain

Tom's business is clearly an active asset and he qualifies under the small business entity test. The 50% active asset reduction applies to the discounted gain.

$275,000 × 50% = $137,500 remaining gain

Tom elects to apply his lifetime retirement exemption of $500,000; more than enough to cover the remaining $137,500. The remainder of the gain is fully exempt.

$137,500 → $0 remaining gain

Because Tom is under 55, the $137,500 retirement exemption amount must be contributed to superannuation. This isn't a penalty, it's actually a benefit. The money goes into super where it will be taxed at a concessional rate and is protected for his retirement.

From 1 July 2027, the general 50% discount is replaced by cost base indexation. Note if you currently own a business you will need to get a valuation on your business for 1 July 2027, as the general discount applies to that date, and then it is the indexation method from 1 July 2027 onward. For our example we are just using the indexation method only to keep the comparison simple.

Consumer Price Index Rates

Tom’s original cost base of $100,000 is indexed for inflation over the 8-year holding period. At 2.5% p.a., his indexed cost base becomes $121,840. Only the real gain above that figure is brought to account.

$650,000 − $121,840 = $528,160 capital gain

The 50% active asset reduction applies in exactly the same way as before - unchanged by the Budget reforms.

$528,160 × 50% = $264,080 remaining gain

Tom still has his full $500,000 lifetime retirement exemption available - more than enough to cover the $264,080 remaining. The gain is fully extinguished.

$264,080 → $0 remaining gain

As before, Tom is under 55 so the $264,080 retirement exemption amount must go into superannuation. Note this is higher than the $137,500 required in the pre-2027 version - because indexation provides less initial relief than the old 50% general discount did for a business that has grown strongly. But the tax outcome is identical: zero.

The Government’s CGT changes simply don’t reach Tom. The small business concessions sit above and outside that regime entirely.

You may have seen the memes. “Albo’s secret 47% partner.” “The government gets half when you sell your business.” They spread quickly on social media after the Budget, and they caused real anxiety among small business owners who’ve spent decades building something.

Here’s the problem with that framing: it describes the maximum marginal tax rate applied to the maximum possible taxable gain, with zero concessions applied. For a high-income individual with no planning and no eligibility for anything, the numbers are roughly correct. For a small business owner who qualifies for the Division 152 concessions? It’s almost completely irrelevant.

The small business CGT concessions are a different regime entirely. They exist specifically because legislators recognised that a business is not just an investment - it is someone’s livelihood, built over years of work, risk, and sacrifice. And they are confirmed unchanged by the 2026–27 Budget. This isn’t spin or optimism - it’s exactly what the Budget Papers say.

For the overwhelming majority of small business owners - the banh mi shop, the panel beater, the bookkeeper who went out on their own - the real story isn’t 47%. It’s zero, or close to it. The key is knowing the rules exist, structuring correctly before you sell, and getting advice early enough to use them properly.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by