Access advice to guide your steps

[et_pb_section fb_built=”1″ _builder_version=”4.6.0″ _module_preset=”default”][et_pb_row _builder_version=”4.6.0″ _module_preset=”default”][et_pb_column _builder_version=”4.6.0″ _module_preset=”default” type=”4_4″][et_pb_text _builder_version=”4.6.0″ _module_preset=”default” hover_enabled=”0″ sticky_enabled=”0″]

The Superannuation Co-contribution Scheme started in 2003/04 to encourage us to make personal contributions to superannuation. It was targeted at low to middle income earners and has been improved progressively since then.

In 2018-19, more than 329,000 Australians claimed over $104 million in co-contributions. A lot of people are taking advantage of this opportunity.

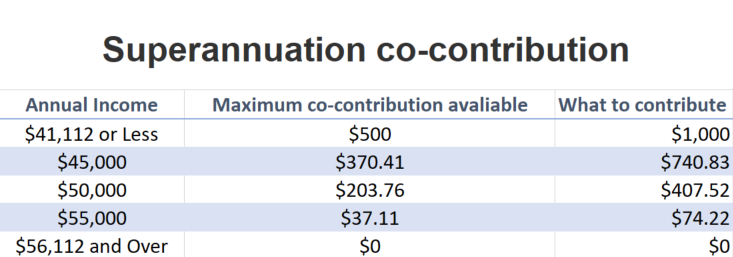

In the 2021-22 year, if you earn an income of $41,112 you can qualify for the maximum co-contribution. (Income = assessable income plus reportable fringe benefits.) The co-contribution reduces by 3.333c in the dollar for each dollar of income over $41,112 and cuts out when your income reaches $56,111.

To be eligible to receive the co-contribution you need to have a total superannuation balance of less than $1.7 million and have not exceeded your non-concessional contributions cap for that financial year.

Outlining the benefit available of the Government Co-contribution scheme and the contribution required to get the benefit.

The co-contribution is also available to self-employed Australians who earn at least 10% of their total income from employment or running a business. (Income = assessable income plus reportable fringe benefits less business income deductions.)

You must make a personal contribution without claiming a tax deduction for it. The Tax Office will work out the co-contribution amount from information on your tax return and details of contributions provided by your super fund.

Here’s a chance to give your children a unique gift.

As soon as they start work they could qualify for the co-contribution. But with retirement a long way off and other priorities (like having a good time) they are unlikely to want to part with $1,000 to pay into superannuation.

But what if you contributed it for them?

Assuming your child is 20 years old and earns less than $41,112, the government would match your contribution with $500. If you repeated this gift for five years and their super earned 7.5% they would have an extra $8,700 in savings. The power of compound interest means that by the time they reach age 60, they would have an extra $109,000 in superannuation!

Read more about this on the ATOs website.

[/et_pb_text][et_pb_cta _builder_version=”4.6.0″ _module_preset=”default” title=”Get the right advice for your financial situation” button_text=”Book a call back now” button_url=”https://calendly.com/fundedfutures/request-a-call-back” hover_enabled=”0″ sticky_enabled=”0″][/et_pb_cta][/et_pb_column][/et_pb_row][/et_pb_section]

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by