Access advice to guide your steps

More than 8 million Australians now rely on some form of income support — that’s nearly one in three working-age people. A new report from the Council of Australian Life Insurers (CALI), produced with Monash University and SuperFriend, found demand has increased across all 11 of Australia’s income support systems, with around 2 million more people accessing payments than a decade ago.

The single biggest driver? Mental health. It now accounts for approximately one-third of all income support claims — and those claims tend to be more complex and last longer than physical injury claims.

For working Australians, this raises an important question:

Most people assume “the government will help.” And yes — there is a safety net. But as this article explains, that net has significant limitations, and the gap between government support and your current lifestyle may be far larger than you think.

When illness or injury stops you from working, you broadly face two scenarios:

– You have income protection insurance, which replaces a portion of your income while you recover.

– You don’t — and you eventually rely on government support, most likely the Disability Support Pension (DSP).

Let’s look at both options honestly.

Income protection insurance pays you a monthly benefit — typically up to 70% of your pre-disability income — if you’re unable to work due to illness or injury. It’s one of the most important yet underutilised forms of personal insurance in Australia.

– Waiting period: Most policies have a waiting period of 30, 60 or 90 days before benefits begin. The longer the waiting period, the lower your premium.

– Benefit period: You can choose how long benefits are paid — 2 years, 5 years, or to age 65. Longer benefit periods offer greater protection but cost more.

– Agreed vs indemnity value: Agreed value policies lock in your insured amount at application; indemnity policies pay based on your income at time of claim.

– Tax deductibility: Premiums are generally tax-deductible when held outside superannuation, and benefits received are assessable income.

The CALI report highlights that mental health claims across Australia have surged — in some age cohorts by more than 730% over 10 years. These claims are now the leading driver of long-term income support nationally. Importantly, quality income protection policies cover mental health conditions, subject to standard policy terms and any applicable exclusions.

This matters because mental health conditions don’t discriminate by industry, age or income level. Your biggest risk may not be a physical accident — it could be burnout, anxiety, depression or a condition like Long COVID.

“Without income protection, I would’ve had to move back in with my parents and be completely dependent again.”

— Lauren Frahamer, 30, former stage manager living with Long COVID

Lauren had a demanding, well-paid career in musical theatre, significant savings, and no reason to expect a health crisis. After contracting COVID-19 in December 2021, she was unable to return to full-time work. Her partial income protection benefit preserved her independence, kept her in treatment, and gave her a pathway back to work — nine hours per week at the time of the ABC report, with a clear goal of returning to full capacity.

The alternative — depleting savings and relying entirely on government support — would have had lasting financial and personal consequences.

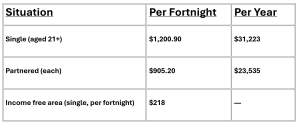

The DSP is a government payment for Australians with a permanent physical, intellectual or psychiatric condition that prevents them from working 15 or more hours per week. It is an important part of Australia’s social safety net. But it is designed as a last resort, not as a replacement for lost income.

Source: Services Australia, 20 March 2026. Rates include base pension, Pension Supplement and Energy Supplement.

Before relying on the DSP as a fallback plan, it’s worth understanding what it actually involves:

– Your condition must be permanent. The DSP is not for temporary illness or injury. Your condition must be fully diagnosed, treated and stabilised, with a functional impairment score of 20+ points on Centrelink’s Impairment Tables. If you’re likely to recover, you may not qualify.

– You cannot work 15+ hours per week. If you’re able to work even part-time at or above minimum wage, you may be ineligible or receive a reduced payment.

– Income and assets tests apply. Your savings, investments and your partner’s income can all reduce your entitlement — or disqualify you entirely.

– The application process is demanding. Medical evidence, Centrelink assessments and ongoing reviews are required. At a time when you’re unwell, this administrative burden is significant.

– Superannuation stops accumulating. With no employer contributions and no compulsory super, your retirement savings take a hit for every year you’re out of the workforce.

Consider a 40-year-old earning $100,000 per year who becomes unable to work:

| Income Protection | DSP Only | |

| Annual income replaced | ~$70,000 (70% of salary) | $31,223 (max, single) |

| Income replacement rate | 70% of pre-disability income | ~31% of prior salary |

| Eligibility hurdle | Unable to perform own occupation (varies by policy definition) | Permanent condition; cannot work 15+ hrs/week at min. wage |

| Waiting period to receive payment | 30–90 days (then benefits begin) | Weeks to months of Centrelink assessment |

| Impact of savings & assets | No effect — benefit based on policy | Savings and assets reduce your payment |

| Superannuation contributions | Often included as a policy benefit | None — no employer, no contributions |

| Duration of support | Up to age 65 (if structured this way) | Ongoing while permanently incapacitated |

| Mental health coverage | Yes, subject to policy terms | Yes, if condition meets DSP threshold |

Note: Income protection figures are illustrative and depend on individual policy terms, waiting periods and benefit periods. DSP figures are maximum rates as at March 2026 and subject to income and assets testing.

The difference between 70% income replacement (~$70,000/yr) and the maximum DSP ($31,223/yr) is approximately $38,777 per year — or $745 per week. Over a 10-year claim, that’s nearly $390,000 in foregone income.

Consider what that difference actually means day-to-day:

– Rent and housing costs in most Australian capital cities are difficult to sustain on the DSP alone, particularly for those without a mortgage-free home.

– Ongoing medical expenses — specialist appointments, medications, allied health — can quickly erode a DSP payment, particularly for complex conditions like mental illness or Long COVID.

– Mortgage repayments don’t pause. A $600,000 mortgage at current rates requires repayments well in excess of the maximum DSP.

– Superannuation erodes year by year. Every year without employer contributions and compulsory super widens the gap at retirement.

The CALI report found close to $80 billion per year is being spent across all 11 income support systems. With demand rising — particularly for mental health conditions — pressure is growing on both government and private systems.

Researchers and life insurers are calling for a government-led overhaul to link Australia’s fragmented income support systems, improve early intervention, and standardise mental health definitions. The underlying message is clear: the current system intervenes too late and costs everyone more in the long run.

This has direct implications for working Australians:

– Government eligibility rules can tighten. DSP access has generally become more restrictive over time, not less. Qualifying is not guaranteed.

– Private insurance underwriting is evolving too. Mental health exclusions, loadings and benefit limitations are common for people who wait until after a mental health episode to apply for cover.

– The best time to apply is when you’re healthy. Waiting until you need it means cover may not be available on the terms you need — or at all.

– If I couldn’t work for 6 months, how long could I sustain my current lifestyle from savings alone?

– Does my super fund include income protection? If so, what is the benefit period, waiting period, and definition of disability?

– If I have existing cover, was it set up based on my current income and financial obligations — or has my situation changed?

– Am I relying on a default super fund IP policy that may have significant limitations on benefit period or definition?

– What would it mean for my family or partner if my income stopped entirely?

| Talk to Your Adviser

Income protection is not a one-size-fits-all product. The right policy depends on your occupation, income, financial commitments, health history and personal goals. A properly structured policy, reviewed as part of your broader financial plan, is one of the most powerful tools available to protect everything you’ve worked to build. We’re here to help you understand your options. Contact us to arrange a review of your current cover — or to explore what’s available if you don’t yet have any in place. |

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by