Access advice to guide your steps

One of the most misunderstood areas of Fringe Benefits Tax (FBT) is private use of employer-provided vehicles. Many business owners assume that “a work car is a work car” — but the FBT rules treat vehicles very differently depending on what type of vehicle it is, how much it cost, and how it’s actually used.

A short commute in one vehicle might be ignored for FBT purposes, while the exact same trip in another vehicle can trigger a full taxable fringe benefit.

This article breaks it down by vehicle type — cars, utes, dual cabs, and luxury cars — and explains what private use is allowed (if any), when FBT applies, and where businesses commonly get caught out.

Before looking at vehicle types, it’s important to understand what the ATO considers private use.

Private use generally includes:

– Travel between home and work

– Travel on weekends

– Travel for personal errands

– Any non-work use of the vehicle

Business use includes:

– Travel between worksites

– Travel to meet clients

– Travel to suppliers or jobs

– Travel undertaken in the course of earning income

However, some private use is treated as minor, infrequent and irregular, and can be ignored — but only for certain vehicle types.

What is a “car” for FBT purposes?

For FBT, a car is broadly any motor vehicle:

– Designed to carry less than one tonne

– Designed to carry fewer than 9 passengers

This includes:

– Sedans

– Hatchbacks

– SUVs

– Wagons

– Many dual cabs (more on that later)

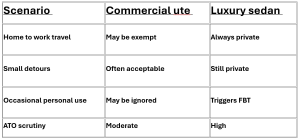

Home-to-work travel = private use

For cars, travel between home and work is always private use. There is no general exemption for commuting, even if:

– The car is branded

– The employee is on call

– The employee stores tools in the vehicle

If a car is available for private use, FBT applies — even if the employee claims they “only use it for work”.

Small detours don’t save you

Stopping briefly on the way home (for example, grabbing milk or picking up kids) does not convert the trip into business travel. It remains private.

FBT calculation applies

Once a car is available for private use, the employer must calculate FBT using either:

– The statutory formula method, or

– The operating cost method (with a valid logbook)

This is where the rules start to differ significantly.

What qualifies as a commercial vehicle?

Vehicles that are not designed primarily for passengers, such as:

– Utes

– Panel vans

– Some dual cabs (depending on payload)

– Trucks

These vehicles can qualify for a FBT exemption for limited private use.

The Limited Private Use Exemption

Under ATO guidelines, certain commercial vehicles can be exempt from FBT if private use is limited to:

– Travel between home and work

– Travel that is incidental to business use

– Minor private use that is infrequent and irregular

This is commonly referred to as the “work-related vehicle exemption”.

What does “minor, infrequent and irregular” mean?

The ATO generally accepts:

– Small detours (e.g. stopping for fuel or groceries)

– Short personal trips (often referenced as up to around 2 km)

– Occasional use that is not routine or planned

What is not acceptable:

– Regular weekend use

– School drop-offs every day

– Using the vehicle as the family car

– Long personal trips or holidays

Once private use becomes regular or substantial, the exemption is lost and FBT applies.

Dual cab utes are one of the most common sources of FBT mistakes.

Why dual cabs are tricky

Dual cabs can be either:

– A commercial vehicle, or

– A car, for FBT purposes

The classification depends on payload capacity, not how it looks.

Payload test (simplified)

If the vehicle’s designed carrying capacity (payload) is:

– More than one tonne → generally treated as a commercial vehicle

– One tonne or less → generally treated as a car

This means:

– Some popular dual cabs qualify for the limited private use exemption

– Others are treated the same as a sedan or SUV

Practical outcome

If your dual cab:

– Qualifies as a commercial vehicle → limited private use (including home-to-work) may be exempt

– Is classified as a car → any home-to-work travel is private use and FBT applies

This distinction alone can be worth thousands of dollars per year.

Luxury cars are where the rules are the strictest — and the most expensive if misunderstood.

What is a luxury car for FBT purposes?

A vehicle that:

– Meets the definition of a car, and

– Has a cost above the Luxury Car Tax (LCT) threshold

(Exact thresholds change over time, but the principle remains the same.)

No special concessions for commuting

For luxury cars:

– Home-to-work travel is always private use

– There is no exemption for limited or incidental use

– Even minimal private availability can trigger FBT

Importantly:

– The ATO applies much greater scrutiny to luxury vehicles

– Claims that the vehicle is “only for work” are rarely accepted without strong evidence

Higher cost = higher FBT exposure

Luxury cars often result in:

– Higher taxable values

– Higher FBT payable

– Reduced deductions (due to cost caps)

In practice, a luxury car provided to an employee almost always results in an FBT liability unless private use is completely restricted and controlled.

Two vehicles used in the exact same way can have completely different FBT outcomes:

This is why FBT planning starts with vehicle selection, not just usage.

Assuming all utes are exempt

Many dual cabs fail the payload test.

Ignoring availability

If the car is available for private use, FBT may apply even if it wasn’t actually used.

No documentation

Lack of policies, logbooks, or usage records makes exemptions hard to defend.

Treating luxury cars casually

These attract extra scrutiny and fewer concessions.

FBT on vehicles is not about intention — it’s about classification, cost, and actual use.

– Commercial vehicles can offer valuable FBT exemptions, if used correctly

– Cars — especially luxury cars — have far fewer concessions

– Small details like payload, cost thresholds, and minor detours can materially change the outcome

Getting this wrong can mean unexpected FBT bills, penalties, and interest. Getting it right can mean legitimate tax savings and fewer compliance headaches.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by