Access advice to guide your steps

For many Australians in their mid-70s, superannuation is still doing exactly what it was designed to do:

providing tax-free income in retirement.

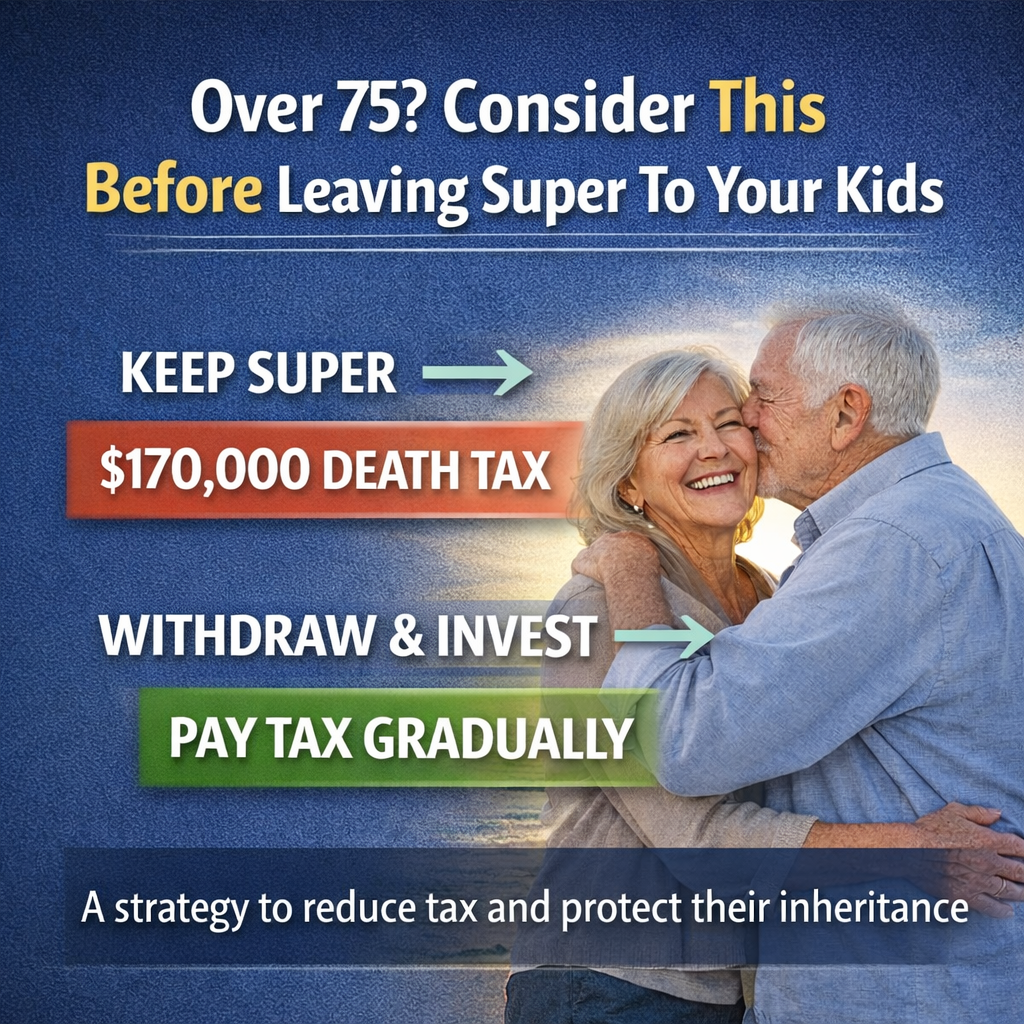

But there’s a problem lurking in the background — what happens when you die.

If your super is paid to adult children (non-tax dependants), the taxable component can be hit with up to 15% plus Medicare levy, collected by the Australian Taxation Office.

On large balances, this can quietly erase six figures from your family’s wealth.

Before age 75, advisers commonly use a recontribution strategy:

But once you turn 75, this strategy is effectively off the table.

So what are you left with?

Let’s work with a realistic scenario.

Client profile

Each child receives roughly $343,000.

That lump sum:

This isn’t just tax — it’s collateral damage across the family’s financial position.

If you have a younger spouse:

Super can roll to them tax-free

The balance continues in pension phase

Death tax may be deferred for decades (until they pass, but they too can get a younger spouse)

Morbid? Slightly.

Effective? Absolutely.

The longer funds stay within the dependant environment, the longer you avoid death tax leakage.

Tax dependants (for super purposes) include:

Financially dependent children

Minor children

Adult independent children do not qualify.

If estate planning flexibility exists, structuring super to first pass to a dependant can reduce or mitigate ALL superannuation tax.

$1.2m withdrawn tax free

Assume a diversified portfolio producing:

$70k p.a. income (mix of dividends + realised capital)

Even at the high end:

$20k p.a. over 10 years = $200k

But this tax:

This option often breaks even or wins over a surprisingly short timeframe.

This is where the strategy becomes far more interesting.

$1.2m withdrawn tax free

Invest how you would normally invest

Company tax rate: 30% (Non-Active Financial Entity)

Franking credits retained inside the company (company tax paid on earnings and realised gains)

Keeping with the $70,000 assumption that is $21,000 in tax paid - avaliable as franking credits each year.

Client draws $70k p.a. (via dividends)

$0 tax paid personally, $11,000 in franking credits used up. (of the $21,000)

But compare the trade-off:

Death tax: ~$170,000 (once, immediately)

Ongoing tax paid gradually

Franking credits preserved

No death tax on principal

Credits survive the client

Even if the company pays:

$15k–$25k p.a. in tax

It takes many years before the total tax paid exceeds the death tax avoided.

Super tax components die with you.

Franking credits don’t.

When the company passes to the children:

They inherit fully franked shares

Credits can be streamed

Income can be distributed flexibly

No forced lump sum event

Compare that with super:

Lump sum

Taxable

No control

No smoothing

Receiving a super death benefit:

Is a single, taxable event

Pushes income higher in one year

Affects means-tested benefits

Can distort family law and support obligations

Receiving wealth via:

Company shares

Gradual distributions

Estate planning structures

Is almost always less disruptive and more efficient.

People fixate on:

“But super is tax free…”

Yes — while you’re alive.

But super was never designed as an intergenerational wealth vehicle.

Once estate planning becomes the priority, structure beats rate.

✔️ It is a trade-off strategy

✔️ It converts one large tax into smaller, controlled taxes

✔️ It prioritises family outcomes over personal tax purity

❌ It is not about eliminating tax entirely

❌ It is not suitable for everyone

❌ It requires modelling, not rules of thumb

After 75:

Recontribution strategies are gone

Flexibility drops sharply

Estate tax risk becomes locked in

Which means the conversation needs to happen now, not later.

If you:

Are over 75

Have a large taxable super balance

Expect super to pass to adult children

Then doing nothing is still a decision — and often an expensive one.

Paying some tax during life may:

Save six figures on death

Preserve flexibility

Protect your children’s broader financial position

Super is brilliant for retirement income.

But once estate planning becomes the goal, it may be time to look beyond it.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by