Access advice to guide your steps

When most people think about investment risk, they picture a graph plunging downward; a portfolio losing value overnight. It’s visceral, it’s memorable, and it keeps billions of dollars sitting in savings accounts and term deposits earning next to nothing. But there’s another risk that never makes headlines, never triggers a news alert, and never causes a moment of panic. It just quietly works against you, every single day. It’s called purchasing power risk; and for the cautious investor, it may be the most dangerous risk of all.

A savings account balance that never drops feels safe. And in nominal terms, it is; the number on your statement either stays the same or grows slightly. But a dollar today does not buy what a dollar bought five years ago, and it won’t buy what a dollar buys today in five years from now. Inflation is the silent erosion of what your money can actually do in the real world.

Consider this: if inflation averages 3% per year, and your savings account earns 1.5%, you are not breaking even. You are falling behind by roughly 1.5% every year. Compounded over a decade, that’s a meaningful and permanent loss of purchasing power; and unlike a market correction, it never bounces back. This is especially relevant when considering the impact on your superannuation balance. Even a seemingly small erosion of purchasing power can significantly impact your retirement savings over the long term. We can discuss strategies like salary sacrifice or additional contributions to help offset this.

The traditional risk spectrum runs from “low risk, low return” on the left (cash) to “high risk, high return” on the right (equities). This framing makes cash look like the safe harbour and equities look like the danger zone.

But what if we measured risk differently? What if, instead of measuring the risk of your balance falling, we measured the risk of your buying power falling?

The picture flips entirely.

Cash in an at-call savings account carries almost no balance risk, but it carries enormous purchasing power risk. Your money is virtually guaranteed to lose real value over time. Term deposits are better, but rarely enough to beat inflation after tax. Remember, interest earned on term deposits is considered taxable income, reducing the net return. We can explore tax-effective investment options within superannuation or outside of it to minimise this impact. Investment-grade corporate bonds begin to get you closer to the inflation line. It’s generally only when you move into diversified growth assets {property, infrastructure, shares} that you consistently have the opportunity to outpace inflation over time and genuinely grow what your money can buy.

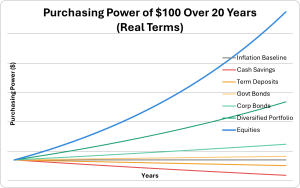

The chart below illustrates this. Notice how the “safe” end of the spectrum is actually where you lose the most purchasing power, and the perceived “risky” assets are the ones that have historically protected and grown it.

Starting with $100 of purchasing power, after 20 years: cash has shrunk to around $74. Term deposits fare slightly better but still leave you behind. Government bonds roughly tread water. It isn’t until corporate bonds and more comfortably, diversified portfolios that you start to see your purchasing power genuinely grow. Equities, despite all the volatility along the way, can more than triple your real purchasing power over two decades.

The volatility of equities is real. There will be years where the balance drops, sometimes significantly. But here’s the critical distinction: that volatility is temporary. The erosion of purchasing power from sitting in cash is permanent and compounding. It’s also important to remember that any capital gains realised from investments held outside of superannuation will be subject to Capital Gains Tax. Proper asset allocation and a long-term investment horizon can help mitigate this. Furthermore, in Queensland, if you were to use investment property, you need to consider Land Tax implications depending on the value of your holdings.

For clients who hold large cash balances, the more useful question is: can I afford not to? The choice isn’t between risk and safety. It’s between two very different types of risk -one that’s visible and frightening, and -one that’s invisible and relentless.

A well-constructed portfolio, matched to your goals, time horizon, and genuine capacity for short-term fluctuations, isn’t a gamble. It’s the deliberate decision to protect what you’ve worked hard to build.

This article is general information only and does not take into account your personal financial situation, needs, or objectives. Before acting on this information, you should consider whether it is appropriate for you and seek advice from a licensed financial adviser. Past performance is not a reliable indicator of future performance.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by