Access advice to guide your steps

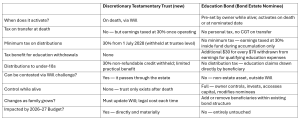

For decades, the discretionary testamentary trust has been one of the most powerful tools in an Australian estate planner’s kit. Established through a Will, it comes into existence on death and has historically allowed the deceased’s estate to distribute investment income to minor beneficiaries — children and grandchildren — at adult marginal tax rates rather than the 47% penalty rate that applies to living trust distributions to under-18s.

That advantage is now gone for anyone who hasn’t died yet.

The 2026–27 Federal Budget confirmed that new discretionary testamentary trusts — those established under Wills written or revised after the Budget announcement on 12 May 2026 — will be subject to the new 30% minimum tax on distributions from 1 July 2028. The income-splitting strategy that made these trusts attractive for passing wealth to younger generations no longer works as designed.

If you are alive today and your Will includes a testamentary trust structure — or you’ve been considering adding one — this Budget requires a direct conversation with your financial adviser and estate planning lawyer about whether your plan still achieves what you intend.

The Budget introduces a 30% minimum tax on the taxable income of discretionary trusts, payable by the trustee from 1 July 2028. Beneficiaries receive a non-refundable credit for the tax paid, which they can apply against their own income tax — but this credit is non-refundable, meaning it can’t create a tax refund for beneficiaries with no other tax liability (such as children).

The Budget papers provide limited relief for existing testamentary trusts: income from assets of a discretionary testamentary trust already in existence at the time of the Budget announcement is excluded from the minimum tax. In plain terms — if the will-maker has already died and the testamentary trust is already operating, it is grandfathered.

But there is no grandfathering for trusts that haven’t been triggered yet.

If you are alive today and your Will instructs that a discretionary testamentary trust be established upon your death, that trust will be a new discretionary trust when it comes into existence — and it will be subject to the 30% minimum tax. The fact that your Will exists today does not protect it.

Fixed testamentary trusts are excluded from the minimum tax, but they solve a different problem. A fixed trust does not allow the trustee to vary distributions between beneficiaries — distributions are determined by the trust deed. This removes the very flexibility that made the discretionary testamentary trust useful for education and intergenerational wealth planning. You can’t direct more income to a grandchild with fees due and less to one who doesn’t need it.

The conclusion is straightforward: for anyone planning to use a testamentary trust structure as a vehicle for passing wealth to children or grandchildren for education purposes, the Budget has removed its primary tax advantage if the will-maker is still alive.

To understand why this matters, it helps to be clear about what the strategy was designed to achieve.

A parent or grandparent accumulates assets during their lifetime. Upon death, rather than assets passing directly to beneficiaries (and potentially being spent or mismanaged), they flow into a trust controlled by a trustee — often a surviving spouse or adult child. The trustee then distributes income from those assets to beneficiaries over time, including to minor grandchildren.

The key tax advantage was that income distributed from a testamentary trust to a child under 18 was taxed at the adult marginal rate applicable to that child’s total income — often zero or 19 cents in the dollar — rather than the 47% penalty rate that applies to the same distribution from a living (inter vivos) trust.

For a grandparent with a $1.5 million estate earning 5% per year, that’s $75,000 in annual income potentially distributed across several grandchildren at very low tax rates. The after-tax income available for school fees, university costs, or a first home deposit was substantially higher than under any alternative structure.

From 1 July 2028, that $75,000 will first have 30% withheld at the trustee level. Grandchildren with no other income will receive a non-refundable credit — meaning they simply absorb the 30% withholding with no ability to recover it. The benefit to younger-generation beneficiaries is materially reduced.

An education bond offers a structurally different approach to the same goal — and it is entirely untouched by the Budget’s trust reforms.

Rather than accumulating assets in an estate and distributing them through a testamentary trust after death, an education bond allows the bond owner to:

Structure the transfer while alive. The bond owner designates Bond Estate Nominees and can set a Future Activated Transfer — a pre-determined instruction for ownership of the bond to pass to nominated beneficiaries at a specified date or upon death. This transfer occurs outside the Will and outside the legal estate entirely. There is no probate process, no potential for legal challenge by other family members, and no delay.

Pass the asset with no tax or CGT event. When an education bond transfers to a nominated beneficiary upon the owner’s death, there is no personal tax liability and no CGT event for either the estate or the beneficiary. The bond simply continues under new ownership. The earnings already taxed inside the fund at 30% during accumulation do not attract any additional tax on transfer — and critically, that 30% is not withheld at the point of distribution to beneficiaries in the way the trust minimum tax operates. The beneficiary inherits the bond intact and can then draw on it for education expenses under the bond’s own tax rules, including the education tax benefit.

Retain control during your lifetime. Unlike a testamentary trust which only activates on death, an education bond is a living investment. The bond owner remains in full control — able to make investment decisions, access capital tax-free at any time for personal use, add or change education beneficiaries, and modify transfer instructions as family circumstances change. The Bond Guardian feature ensures someone trusted can administer the bond if the owner becomes incapacitated before death.

Avoid the estate entirely. Because the bond passes as a non-estate asset, it does not form part of the Will. It cannot be delayed by probate, contested by disappointed beneficiaries, or disrupted by family law proceedings. For families where estate conflict is a concern — second marriages, blended families, estranged relatives — this is a significant practical advantage alongside the tax benefit.

The testamentary trust and the education bond are trying to achieve the same outcome: getting accumulated family wealth into the hands of the next generation in a tax-efficient way, earmarked for education and life events. After this Budget, one of those tools has had its primary tax advantage removed for anyone who hasn’t yet died.

This is not an abstract planning consideration. Anyone in the following situations should be reviewing their position before their Will becomes the operative document:

Parents with a testamentary trust clause in their Will. If your Will currently includes a discretionary testamentary trust, the tax advantage that justified including it has been removed for trusts that come into existence after Budget night. This doesn’t mean the trust provision should simply be deleted — the control and asset protection features remain valid — but the design, and whether an education bond provides a more effective path to the same outcome, warrants review.

Grandparents planning to leave an inheritance for grandchildren’s education. The testamentary trust was often the vehicle of choice for this. It no longer delivers the tax outcome it once did. An education bond established and funded now, with Bond Estate Nominees set to grandchildren, achieves the intended outcome more cleanly — and because contributions are made during the owner’s lifetime, the bond grows and compounds for longer before it’s needed.

Anyone with blended family or estate conflict considerations. The non-estate nature of the education bond becomes more valuable, not less, in complex family structures. The testamentary trust is exposed to Will challenges in a way the bond is not.

Anyone whose Will hasn’t been reviewed recently. Estate planning documents generally need to be reviewed when legislation changes. The 2026–27 Budget is a trigger — particularly for the testamentary trust provisions that many Australians’ Wills include as a matter of course.

If your Will contains a discretionary testamentary trust provision and you do not update it before you die, the trust will still be established — it will simply operate under the new 30% minimum tax rules when it comes into existence. Your intended beneficiaries will not receive the tax outcome you planned for.

If you die after 1 July 2028 under a Will written before Budget night that you never updated, the grandfathering does not protect you. The grandfathering applies to trusts existing at announcement — not trusts established under Wills written before announcement.

This is worth stating plainly, because many clients assume that a Will drafted years ago with good tax advice reflects the current law. It doesn’t, as of Budget night 2026.

The 2026–27 Budget has fundamentally changed the calculus of testamentary trust planning for education and intergenerational wealth transfer. The mechanism that made discretionary testamentary trusts valuable — the ability to distribute to younger-generation beneficiaries at low or zero effective tax rates — has been removed for any trust yet to come into existence.

The education bond achieves the same underlying goal — accumulating family wealth and distributing it for education and life events across generations — through a structure that is entirely outside the new trust tax regime. It passes on death without tax, without probate, and without contest, to whoever the owner has chosen.

For anyone whose estate plan includes a testamentary trust for these purposes, the conversation with a financial adviser and estate planning lawyer is overdue.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by