Access advice to guide your steps

A “second super tax” takes shape: what’s changing with Div 296

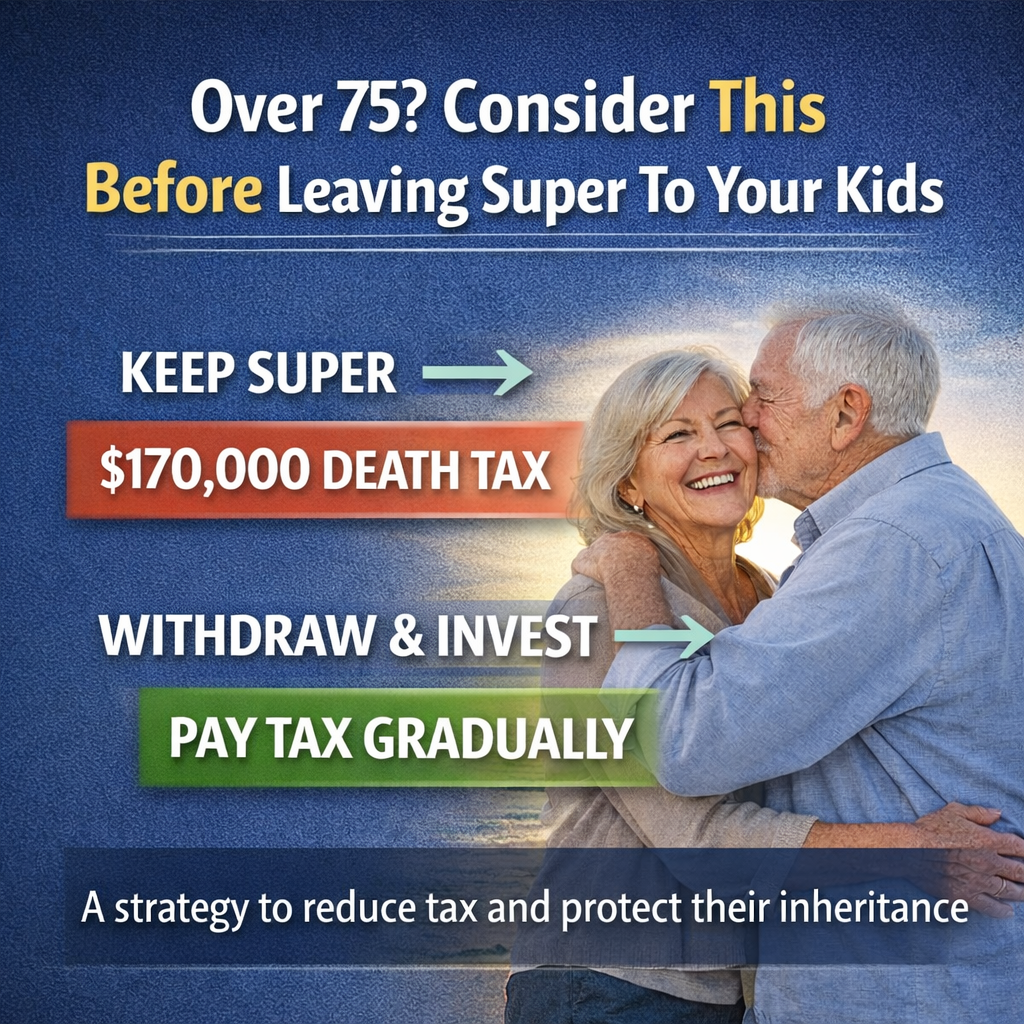

The government’s flagship reform to high-balance superannuation accounts is the Div 296 tax, intended to apply to individuals with total superannuation balances (TSB) above $3 million. Originally the design introduced a 15 % additional tax on earnings (including unrealised gains) attributed to the portion of a balance above $3 m.

However, under recent industry and political pressure the government appears to be modifying both the formula and mechanics of how the tax will operate.

Key reforms under review

Here are the most important changes now on the table:

Why it matters (and how it may affect you)

For individuals (including SMSF trustees) with superannuation balances approaching or above $3 million, these changes introduce considerable strategic implications:

While the core concept of Div 296 remains — an extra tax on superannuation earnings for those with high balances — the mechanics are shifting under pressure. The government appears to be responding to industry concerns around fairness (unrealised gains), indexing, and implementation timing. For those likely impacted, this is not a reason to ignore the reform: rather, it signals the time to engage with advisors, update strategy, and model scenarios under both the original and revised proposals.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by