Access advice to guide your steps

On 19 June 2026, Prime Minister Anthony Albanese and Treasurer Jim Chalmers stood at a Sydney press conference and announced two significant retreats from the 12 May budget. This post sets out exactly what changed, why it matters, and what it means for the articles and guidance we published over the past few weeks. We'll be updating those posts with forward links, but this is your one-stop summary.

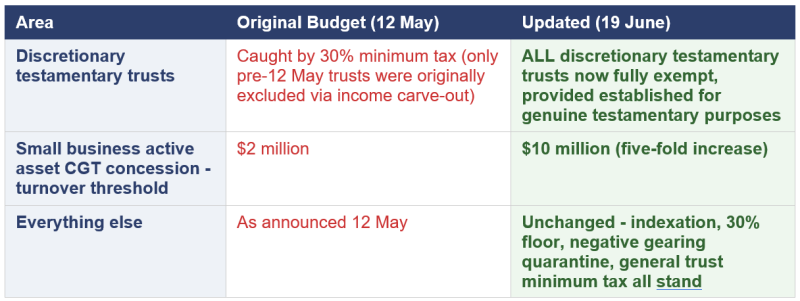

The original budget position on the 30% discretionary trust minimum tax included an income carve-out for "existing testamentary trusts" - meaning trusts that were already operating as at Budget night (12 May 2026). That left a significant gap: testamentary trusts established under Wills written by people who are still alive would not yet exist as trusts, so they fell squarely within the new minimum tax. The only way to be protected was to already be dead; which is a fairly niche planning strategy.

We flagged this issue in detail in our estate planning briefings.

The government has now confirmed that income from ALL types of discretionary testamentary trusts will be exempt from the 30% minimum tax - provided they are established for genuine testamentary purposes. This covers:

- Trusts already operating (as was always the case under the budget carve-out)In other words, the grandfathering gap is gone. The government has addressed integrity concerns through a separate anti-avoidance mechanism rather than by keeping testamentary trusts inside the tax.

For clients with Wills that include testamentary trust provisions, or clients we have been advising to consider testamentary trust structures, this is good news. The structure remains fully viable as an estate planning tool going forward.

A few things are still worth monitoring:

The phrase "genuine testamentary purposes" will need to be defined in legislation. The government hasn't released an exposure draft on the trust minimum tax yet, so the detail of what anti-avoidance provisions look like is still to come.The small business CGT concessions under Division 152 of the ITAA 1997 have always been separate from the general 50% CGT discount - they're an additional layer of relief for qualifying business owners, not a replacement for it.

The main concession relevant here is the active asset reduction: a 50% reduction in a capital gain on the sale of an active business asset. To access it, the entity (or its connected entities) needed to have an aggregated annual turnover of less than $2 million, or satisfy a maximum net asset value test of less than $6 million.

The original budget left Division 152 intact, the small business concessions were explicitly preserved. We made this point in our post debunking the "47% silent Albo partner" social media meme. But the $2 million turnover threshold was unchanged, which meant that many genuine small and medium businesses — particularly those that have grown over the years — couldn't access the active asset reduction at all.

We covered the small business CGT concessions in detail here.

The turnover threshold for the active asset 50% reduction has been lifted five-fold, from $2 million to $10 million.

According to Chalmers, this means approximately 98% of all active Australian businesses will now be eligible for the CGT concession on sale of active assets.

This is a meaningful change for business owner clients, particularly those who:

- Have been building their business for years and now have turnover between $2M and $10M

On the numbers, the active asset reduction stacks on top of the new indexation framework. So from 1 July 2027, a qualifying business owner selling an active asset would first index the cost base (removing the CPI component from their gain), then apply the 50% active asset reduction to the remaining real gain, and then be subject to the 30% minimum floor if the result is below that.

The core architecture of the 12 May budget remains intact. These are not up for negotiation:

- CGT: Cost base indexation replaces the general 50% discount from 1 July 2027The legislation is still before a Senate inquiry and the government is targeting passage within the next fortnight. The trust minimum tax exposure draft has not yet been released.

The direction of these changes is positive, but they don't change the fundamentals. If you hold assets in an ordinary discretionary trust, the 30% minimum tax is still coming in 2028. If you own residential investment property, negative gearing is still being quarantined. If you're planning to realise a large capital gain, indexation will replace the 50% discount from mid-2027.

What has changed is that two groups now have substantially more clarity and certainty than they did on Budget night:

- Testamentary trust clients: Families with estate planning structures built around testamentary trusts, your structure is safeAs always, these are general observations. The right answer for your situation depends on your specific circumstances, entity structure, timing, and objectives. If any of these changes affect planning we've discussed, reach out and we'll work through what it means for you specifically.

This website may contain general advice, but does not take into account your objectives, financial situation or needs. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. In the event that Funded Futures Financial Services is providing personal advice it will be communicated via a ‘statement of advice’.

Funded Futures Financial Planning ABN 81 646 656 804 T/A Funded Futures Financial Services is a Corporate Authorised Representatives and is authorised through Cobalt Advisers Pty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licencee # 512550.

© 2024 Funded Futures | All Rights Reserved | Developed by